Table of Contents:

- What Is Embedded Insurance?

- Introduction

- Why Is Embedded Insurance Growing So Rapidly Today?

- How Embedded Insurance Evolved from Point-of-Sale to Full Integration

- What Makes Embedded Insurance a Trillion-Euro Opportunity?

- Can Embedded Insurance be key to Bridge the Insurance Protection Gap?

- Insurers’ Embedded-Insurance Playbook

- Why AdInsure?

- Conclusion

What Is Embedded Insurance?

Embedded insurance meaning refers to the integration of protection directly into customer journeys, so that coverage is offered at the point of need, rather than being purchased separately.

- Instant Convenience: Customers receive tailored insurance offers (e.g., warranties at checkout or liability cover at rental) and an improved buying experience.

- Data-Driven Personalisation: Real-time transaction and behavioral data let insurers customize coverages and pricing on the fly.

- New Revenue Streams: Businesses and carriers both unlock upsell and cross-sell opportunities right where purchase intent is highest.

Introduction

Embedded insurance is no longer a sideshow; it is racing into the mainstream. Analysts expect global premiums to rise from USD 210.9 billion in 2025 to nearly USD 1 trillion by 2030, a blistering 35% CAGR. Europe is matching that pace, scaling from €10.9 billion to €49.4 billion over the same period.

Two forthcoming EU regulations will pour even more fuel on the fire:

- FIDA (Financial Data Access Regulation) will extend PSD2-style data-sharing to insurance, mandating open-standard APIs and making plug-and-play cover the norm across apps and platforms (EC proposal COM (2023) 360).

- DORA (Digital Operational Resilience Act), effective 17 January 2025, imposes tougher cyber-resilience rules on all financial entities, including insurers, boosting trust in fully digital distribution (EIOPA overview).

With these tailwinds, ecosystem partnerships are poised to thrive, and insurers that can embed friction-free protection where customers already are will capture the next wave of growth.

Why Is Embedded Insurance Growing So Rapidly Today?

Five powerful trends are propelling embedded insurance from niche experiment to everyday expectation across EMEA, boosting customer loyalty and streamlining the insurance purchase journey:

1. API-first distribution (Tech)

Advances in technology mean standard, low-latency APIs let any platform quote, bind, and service an insurance offering in milliseconds. Spain’s Vueling integrates Cover Genius’s XCover API directly into its booking flow to surface relevant insurance coverage at checkout with a single click.

2. Real-time data & micro-duration cover (Micro-mobility)

Telematics and IoT streams enable pay-as-you-ride insurance coverage. Each time a user unlocks a Bird e-scooter, an Allianz liability and personal-accident policy binds automatically; coverage starts at “ride begin” and ends when the scooter is parked, all within the app. This micro-duration model transforms the insurance purchase into a seamless, context-driven experience within mobility distribution channels.

3. Embedded parametric claims & instant settlement (PropTech)

When corporate clients subscribe to Previsico’s flood-monitoring service, they automatically acquire a parametric cover from Descartes; no separate application is required. As soon as IoT sensors detect flood levels breaching the threshold, the policy triggers and the payout arrives instantly in the same dashboard. This friction-free claims flow shows how embedded insurance can elevate any partner’s offering within real-time digital ecosystems.

4. Ecosystem loyalty & new revenue (Telco, Retail, Finance)

Non-insurance brands, especially telecoms, e-commerce platforms, banks, and mobility services, embed peace-of-mind protection to deepen engagement and unlock fresh income. Germany’s O2 Telefónica bundles ERGO’s mobility and travel cover into its O2 Care mobile plans, driving customer loyalty and boosting ARPU through innovative distribution channels.

5. Contextual, frictionless experience (Digital-native expectations)

Today’s users expect any add-on, including insurance, to appear seamlessly in the flow they are already in. Digital banks like Revolut prompt customers to enable travel cover at the point of booking, with pre-filled trip details and one-tap activation. This in-context convenience turns embedded insurance into a must-have feature within modern digital ecosystems.

For customers, these advances in technology make embedded insurance coverage appear exactly when it is relevant, without extra forms or separate portals. Adoption climbs and protection gaps shrink. For partners and insurers, this approach slashes distribution costs, enhances the insurance offering, and fosters lasting customer loyalty throughout the purchase lifecycle. Everyone wins.

.png?hsLang=en)

How Embedded Insurance Evolved from Point-of-Sale to Full Integration?

Embedded insurance began as a simple add-on at the cash register. Over time, technology and shifting customer expectations have driven it toward seamless integration so profoundly that standalone policies already feel out of place.

Early Bundles: Sales Add-Ons (1860s–1990s)

Travel agencies in the late 1800s started bundling trip-cancellation and medical cover with a plane ticket sale. By the 1990s, electronics retailers offered extended warranty plans at checkout process stations—early hints at integrating protection into commerce.

Digital Redirects: Online Links & Pop-Ups (2000s–2015)

Websites used “Buy Insurance” links and post-purchase pop-ups that sent customers offsite to insurer portals, interrupting the checkout process and adding friction to the claims process.

Inline Offers & Parametric Trials (2015–2022)

Insurance options appeared directly in carts and booking flows. Airlines began offering trip cover alongside every plane ticket, and early parametric pilots—for weather events or flight delays—proved event-driven cover works.

API-First Integration: Instant Cover (2022–Today)

Partners like Vueling × Cover Genius and Bird × Allianz use APIs to quote, bind, and service policies in milliseconds. Usage-based and micro-duration covers run entirely in-app. Banking customers life insurance features also emerged, letting banking app users add term or life insurance options alongside other financial products.

One-Tap Activation & Embedded Claims (2025+)

The next frontier embeds insurance completely into partner apps. Revolut already offers one-tap travel cover in its banking app, and parametric claims process flows fire the instant an IoT sensor detects a trigger.

As this evolution shows, protection is becoming so deeply woven into products and services that pausing to buy separate coverage will soon feel unnatural—customers will simply expect insurance as a built-in feature.

According to Simon Torrance, a Senior Partner at ARK: “We are still very much in the early stages of a market opportunity which has very significant potential but which is still very poorly understood, not only by non-insurance companies but also by insurance incumbents themselves.”

What Makes Embedded Insurance a Trillion-Dollar Opportunity?

Embedded insurance sits at the intersection of untapped market potential, fresh distribution channels, and evolving customer behavior, and it builds on Business Insurance Basics by turning risk cover into a seamless service rather than a standalone sale.

1. Massive Global Upside

By 2030, embedded insurance is projected to generate US $700 billion in premiums globally—up from around US $70 billion in 2020—according to Deloitte Insights, underscoring how life insurance companies and P&C carriers can tap new revenue streams through non-traditional partners.

2. Massive European Growth

Europe’s embedded segment is forecast to grow from €10.9 billion in 2025 to €49.4 billion by 2030 (35 % CAGR), driven by fintech, e-commerce, and community-embedded insurance solutions in local markets (Mordor Intelligence – Europe Embedded Insurance Market).

3. New Distribution Channels

Banks, e-commerce platforms, mobility services, telecom operators, and even smart-home security systems are embedding cover at checkout or within their apps. These partners drive scale, lower customer-acquisition costs, and boost customer retention by adding value to existing services (EY – How Insurers Can Win in Embedded Insurance).

4. Seamless Customer Journeys

Modern consumers expect one-click, contextual experiences, from adding coverage to a plane ticket to topping up life insurance in their banking app. Embedded insurance streamlines both the checkout process and the claims process into frictionless, in-flow moments (Accenture – The Seamless Insurance Experience).

5. Technological Integration and Ecosystem Innovation

API-driven technological integration allows insurers to plug into any digital ecosystem. As platforms—from ride-hailing apps to home-security dashboards—mature, insurance becomes a native feature that locks in customers and deepens loyalty (Forrester – The Forrester Wave™: Embedded Insurance, Q3 2024).

This combination of under-penetration today, strong growth forecasts, diverse distribution channels, and rising expectations makes embedded insurance a massive, and still early, opportunity for insurers and their partners.

Can Embedded Insurance be Key to Bridge the Insurance Protection Gap?

The Protection Gap Problem

The aftermath of a recent natural disaster in my country highlighted a pressing concern: the insurance protection gap. This gap reflects the difference between economically and socially necessary coverage and the amount actually purchased. According to Swiss Re’s 2024 Sigma report, the global protection gap stands at USD 1.2 trillion (Swiss Re: Protection gap remains at an estimated US 1.2 trillion).

Why Traditional Channels Fall Short

Decades of reliance on agents and brokers have left many regions underserved. High overhead costs, complex underwriting, and limited distribution in rural or low-income areas prevent millions from securing adequate cover. When disaster strikes, affected households often lack any form of insurance, deepening economic and social strain.

Reaching rural and low-income populations

Today, Mobile platforms now cover 344 million people with microinsurance across 37 countries (Microinsurance Network). Embedding basic health or life cover into mobile top-ups lets rural users buy protection in small increments without paperwork. Likewise, Parametric crop cover uses satellite and weather data to trigger automatic payouts when drought or excess rain hits thresholds. A Sigma report finds 60 % of insurable crop production was uninsured in 2022, a USD 113 billion gap. Embedding this cover in seed or fertilizer sales drives over 60 % uptake, with payouts sent straight to farmers’ mobile wallets.

Community-Embedded Micro-Life Insurance

In parts of Africa, platforms like BIMA (e.g., BIMA Ghana) partner with telecom operators to embed micro-life and health insurance cover into prepaid airtime bundles. Subscribers receive coverage automatically for a nominal daily premium deducted from their airtime balance, leveraging existing billing relationships to reach customers who would never visit an insurance office.

Building Trust Through Familiar Channels

Grocery stores, agricultural cooperatives, and microfinance lenders often have deep relationships in rural areas. By embedding small-sum insurance (for livestock, crops, or personal accidents) into everyday transactions such as paying for seeds or grain, these partners help customers learn insurance benefits in a trusted setting. Over time, positive experiences drive word of mouth, helping communities to become comfortable buying insurance which drives adoption rates.

Limitations & Next Steps

While embedded insurance can close many protection gaps, it is not a panacea. Complex, high-risk lines (e.g., large commercial property) still require traditional underwriting. Going forward, insurers must expand API availability, forge partnerships in emerging markets, and collaborate with regulators to ensure broad, secure access.

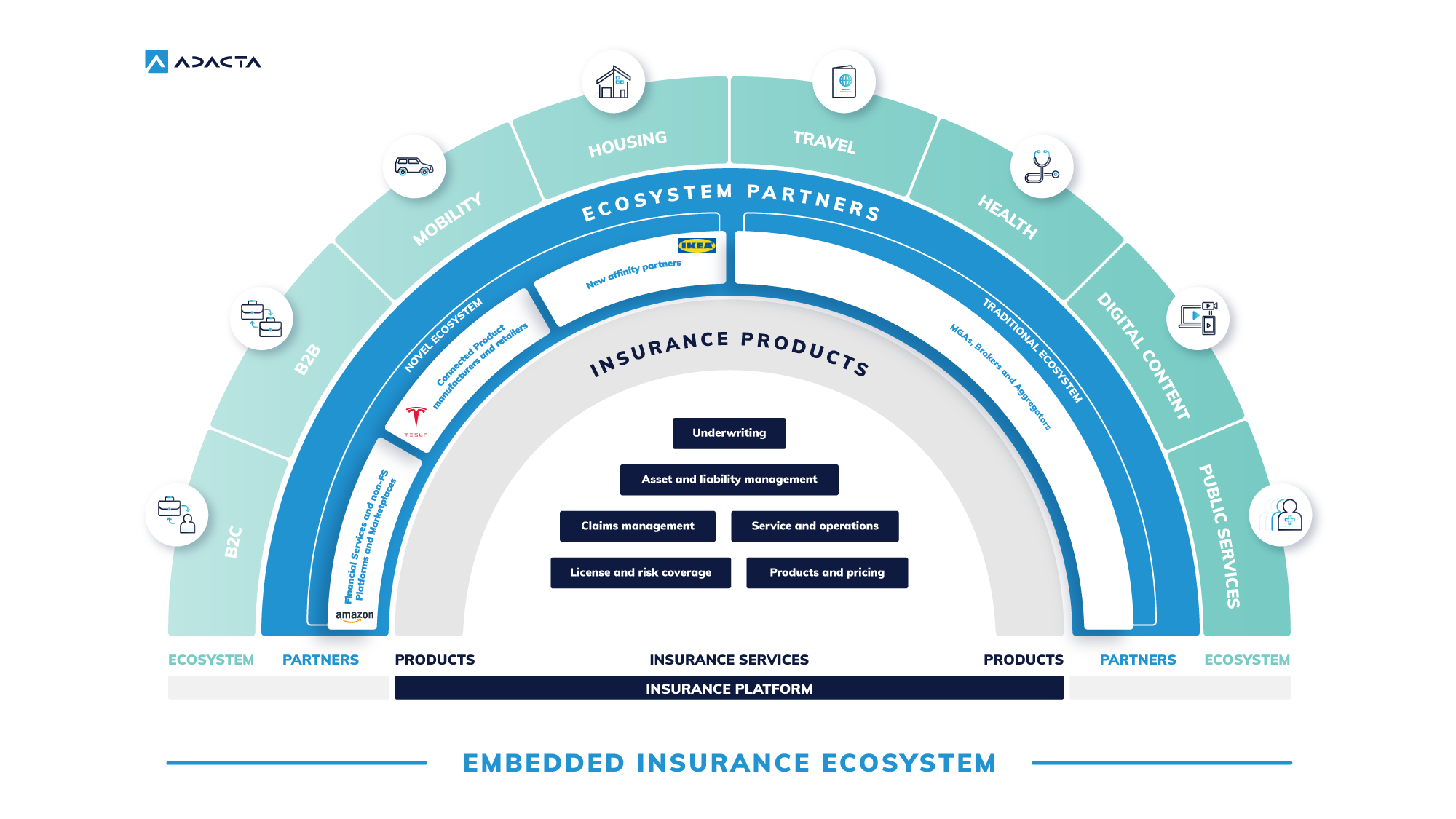

Insurers’ Embedded-Insurance Playbook

What insurers must consider in the embedded space revolves around three pillars: ecosystems (insurance and non-insurance ecosystems), focus, and personalization. Diving into the current landscape, the Asia Pacific market emerges as a frontrunner in embedded insurance adoption. A recent article by McKinsey delves into the rise of embedded insurance in the Asian insurance market, spotlighting the potential advantages for insurers.

To thrive in this evolving space, McKinsey outlines several pivotal capabilities for insurers:

- Partnership development: Building strong alliances with digital platforms is paramount.

- Digital journey design: Insurers must craft a frictionless customer experience, encompassing purchasing, managing, and claiming processes.

- Digital-ready product development: The emphasis is on creating modular and flexible products to expedite the shift towards embedded insurance.

- Robust data and technology: A solid technological foundation is essential for seamless integrations. Solutions like AdInsure facilitate this by ensuring smooth integrations and automating data flows.

- Innovative risk assessment: The embedded model revolutionizes customer data collection, prompting a shift towards proactive coverage strategies.

Why AdInsure?

AdInsure is built for insurers aiming to lead in embedded insurance. Its API-first, cloud-agnostic core lets you launch new products in weeks and plug into any digital ecosystem without ripping out legacy systems. Whether you need to serve banks, e-commerce platforms, telcos, or mobility services, AdInsure provides the flexibility, scalability, and partner-management tools required to embed insurance seamlessly.

Key Capabilities

1. API-First Architecture

AdInsure exposes every function, from quote, rating, binding, claim via modern RESTful APIs. Instead of writing custom integrations for each partner, you simply grant API access and let them pull exactly what they need in real time.

2. Product Configurability & White-Labeling

A low-code product studio lets you assemble modular insurance offerings such as parametric flood cover, pay-per-mile auto policies, micro-duration e-scooter insurance. Tweaking them for each partner is also easy. You can clone a base product, adjust pricing rules or coverage limits, and roll it out under the partner’s brand.

3. Partner Management & Distribution Channels

AdInsure comes with a built-in partner-management features. You can onboard new distributors (banks, retailers, or mobility platforms), manage commissions, track sales metrics, and enforce compliance rules all in one place. Automated billing and revenue-sharing workflows mean fewer manual reconciliations.

4. Data-Driven Underwriting & Parametric Claims

By ingesting partner data (purchase details, telematics feeds, or IoT signals) AdInsure’s underwriting engine can auto-bind low-touch policies. For parametric products, it integrates with event data sources (weather APIs, flight-status feeds, etc.) to trigger instant, predefined payouts. Also Claims workflows can be fully embedded in partner apps.

For a detailed breakdown of how AdInsure reinforces the essential capabilities for embedded insurance, refer to the tables below.

Table 1: Embedded Insurance Business Model Examples

| Capability | Description | Benefit |

| API-First Integration | Expose quoting, binding, servicing, and claims via RESTful APIs. | Enables real-time, seamless embedding inside partner apps. |

| Configurable Product Studio | Low-code interface to assemble and tweak modular insurance offerings for different partners and use cases. | Reduces time-to-market for new embedded products. |

| Partner Management Dashboard | Centralized features to onboard partners, track performance, manage commissions, and enforce compliance. | Simplifies scaling to multiple distributors with minimal effort. |

| Parametric Trigger Engine | Integrate with IoT, satellite, or event data sources to auto-trigger payouts when predefined conditions occur. | Accelerates claims settlement and enhances customer trust. |

| Cloud-support | Deploy on cloud infrastructure and scale based on demand. | Ensures high availability and handles peak quote volumes without degradation. |

| Embedded Claims Workflow | In-app or in-partner UI for policyholders to file or process claims directly within the same platform. | Eliminates portal redirects and reduces claims processing time. |

Table 2: Technical Capability Matrix for Embedded Insurance Platforms

Future Trends in Embedded Insurance — 2025 → 2030

- Open-Insurance APIs Become the Default

The EU’s new Financial Data Access Regulation (FIDA) will extend PSD2-style data-sharing to insurance, forcing standardized, secure APIs by 2027 and making “plug-and-play” cover possible in any app. Milliman - Broader Ecosystems Drive Premium Growth

Analysts expect up to 30 % of European P&C premiums and 10 % of life policies to flow through retail, mobility, fintech and health platforms within the next decade. - Real-Time, Usage-Based & Parametric Cover

IoT, telematics and live event feeds now trigger instant payouts for flight delays, bad weather or pay-per-mile driving—no claims form needed. - AI-Powered Hyper-Personalisation

Advanced ML models fuse partner data with behaviour signals to tailor price, coverage and messages for each user in real time. - Digital Resilience & Compliance

DORA (in full from Jan 2025) and updates to IDD will hard-wire cyber-resilience, transparency and consumer protection into every embedded journey, boosting trust. - Low-Code “Product Factories”

Flexible cores let insurers assemble modular policies, white-label them for partners and launch in weeks instead of months. duckcreek.com

Conclusion

Embedded insurance isn’t new, but it’s come alive again thanks to advances in core technologies, especially API adoption. These innovations make it possible to weave insurance seamlessly into every stage of the customer journey across industries that have never sold insurance before.

The opportunity is huge, but it comes with challenges. Insurers must rethink their business models and dive deeper into partner ecosystems. That means forging collaborations with manufacturers, retailers, and other financial services providers and moving away from a centralized sales approach. Insurers who adapt and innovate in this evolving landscape will be the pioneers of the embedded era, with the opportunity to transform the insurance landscape completely.