Imagine if you could cut the operational costs of handling claims by 30%. It might sound outlandish, but in reality, it’s something you could achieve by focusing on the right thing – using digital technology to modernize your processes.

While insurance was relatively slow in adopting digitalization, the rise of digital technologies has started disrupting the insurance industry after COVID-19. We are no longer talking just about digitizing paper forms and optimizing operations. Instead, digital transformation is driving the emergence of new business models and revenue streams and improved customer experiences. This change is powered by innovative technologies and digital ecosystems that extend insurers' reach into new markets and open up unique growth opportunities.

This post looks at some of the benefits and gives a real-life example of claims digitalization to showcase the benefits of digital technologies powering digital transformation in the insurance sector.

Table of Contents:

- The transformation of insurance

- The three key objectives of digital transformation in insurance

- Digitalization is about the transformation of the Insurance Value Chain

- There are many measurable benefits of digital transformation

- The real-life example of claims digitalization

- The technology you need

- Our own track record with AdInsure

The transformation of insurance – from building digital capabilities to digital innovation

As a technology vendor, we discuss the digitalization of insurance every day with our clients and partners; it is critical to speak the same language and clearly define how digital transformation is supported by our insurance platform AdInsure.

As the industry has still not settled on a common vocabulary, let’s first take a look at how we defined the terms and different levels of digital transformation.

The three key objectives of digital transformation in insurance

Our mission is to support our clients on their quest to remain relevant and gain a competitive advantage in this interconnected and technology-driven customer and business environment. We help them do business in a new way, extending beyond just using technology to improve operational efficiencies and cut costs. Instead, digital insurance accelerates the delivery of new experiences and drives new sources of revenue across new channels.

We see digital strategy as a key driver for achieving three main goals.

- Income from new models. When we talk about revenue, we talk about doing more business over non-traditional insurance distribution channels and insurance intermediaries. This means new self-service and online insurance sales models coupled with virtual online support from agents. It also means ecosystems that plugin more services and products from third parties to deliver more value to your customers.

- Optimization of everything. Optimization can be a straightforward optimization of core processes such as claims or distribution costs. But there are also more advanced scenarios, such as leveraging advanced analytics and machine-learning models to drive better predictions and decisions across the insurance value chain. For example, technology can help you price the risk or assess the complexity of a claim.

- Improved user experience. Customer behavior and expectations have soared over the past couple of years. In a world where Amazon, Google, or Uber have set expectations, no one can expect to get away with a subpar user experience. Customers expect user-friendly experiences that are personalized and transparent.

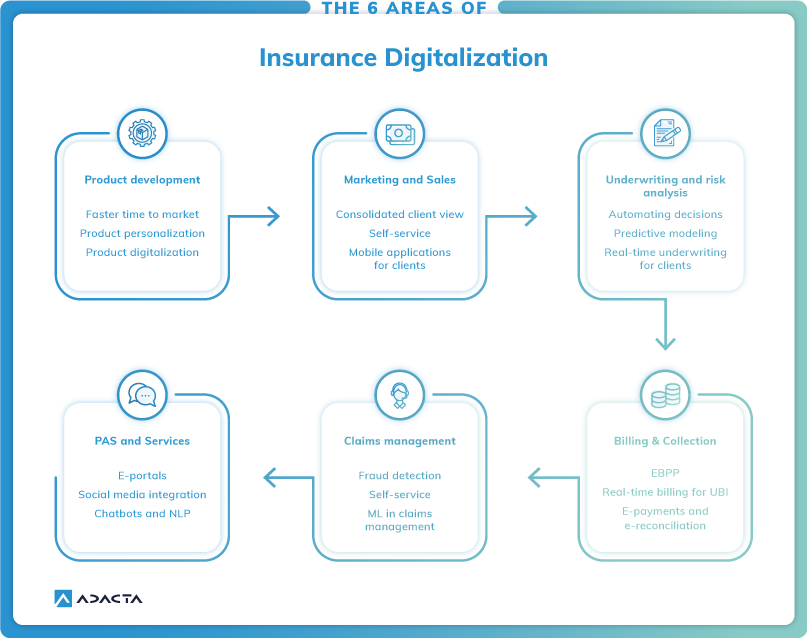

Digitalization is about the transformation of the Insurance Value Chain

The insurance business model or the value chain consists of six key areas, from product development to services. Digitalization of insurance is about transforming these key business areas with the help of technology.

That’s as simple a definition of insurance digitalization as it gets.

The insurance business model starts with product development and sales & marketing. We see a trend and lots of interest in digital interactions and insurance product digitalization, which is all about sales and distribution through digital channels. This is an example of a feature that heavily depends on a modern insurance system that provides the APIs needed to distribute products quickly and efficiently through channels and partner ecosystems.

The next links in the value chain are underwriting and risk analysis, billing and collection, claims management, policy management, and services. Most of these can be digitalized or automated in some way or another.

For example, when it comes to underwriting innovation and risk analysis, numerous decisions can be automated through AI, which can also be used for predictive modelling and real-time underwriting.

This shift is driven by several factors, including data availability, machine, and deep learning, and real-time data processing, enabled by technological advances.

Services can also be delivered more efficiently through digitalization. Technologies, such as self-service portals, paperless services, and chatbots drive productivity and customer satisfaction. By redesigning customer journeys, insurance organizations can profoundly change how they interact with their customers to deliver experiences that meet modern demands.

There are many measurable benefits of digital transformation

Let’s look at some measurable benefits of digitalization as recorded by leading industry consultants and analysts.

KPMG found that “digitally mature organizations had 25% higher revenue growth and 31% higher EBIDTA over the last three years, 11% higher net promoter score and accelerated speed to market by 17 months”.

McKinsey study on digital disruption in insurance estimates that automation can reduce the cost of a claims journey by up to 30%. Technology investments can improve their customer retention and employee satisfaction once they no longer have to perform dull manual tasks.

A Deloitte survey found an overall 30% improvements in underwriting process after insurers moved the entire process online. In the same survey, there is an example of a Chinese insurer using automation to cut the average turnaround time for underwriting from 3.8 days of manual underwriting to 10 minutes.

Ecosystems matter as well. A study by Bain discovered that users are increasingly looking for ecosystem services and are prepared to switch providers for them. In the UK, 61% of consumers are willing to switch providers. These percentages are somewhat lower in mainland Europe but still quite high, reaching 45 and 44 percent in Germany and France respectively.

The real-life example of claims digitalization

Claims are important because they are the number-one cost center (75% of P&C insurers’ cost structure) for insurers while also having a major impact on customer satisfaction and retention (EY Global Consumer Insurance Survey shows 87% of customers say their claims experience impacts their decision to stay with an insurer).

Digitalization of Claims processing allows insurers to:- Improve customer experience and satisfaction

Welcome to the world of chatbots. Sometimes a simple chatbot is all you need. A user logs onto the self-care portal and submits the First Notice of Loss (FNOL) through the integrated chatbot. Chatbots are a great way to offer support that is available 24/7. The chatbot guides the conversation to collect basic information about the claim and automatically creates a new case in the system.

Welcome to advanced claims automation. Some claims cases can be fully automated, as in travel insurance – a cancelled flight triggers a process that can be completed without intervention from the handler or the client.

What it takes is a claims system that provides flexible workflows and process automation via business rules and decision automation – something we offer with AdInsure.

Improve the claims team’s productivity and reduce costs

The key thing here is to give client service representatives a single interface that provides 360-degree information about their clients, tasks, and documents. From this dashboard, they can easily collaborate with other people on their team, the agency, or their customers. A flexible solution will enable them to communicate using chat, e-mail, comments on documents, or video calls. Another important productivity driver is the ability to implement workflows that guide the service representative through the individual steps they need to take.

The technology you need

Your digitization strategy needs to be supported by powerful technology that will allow you to execute against your business goals. When evaluating digital solutions and technologies (whether for private lines such as auto insurance or commercial lines), you should look at the following:

- Software for digitizing your data and digitalization of processes. They usually come in the form of core insurance systems that cover Policy Administration Systems, Claims management, and Billing.

- Insurance platforms for digitalizing your products and integrating with ecosystems, distribution and service partners. They usually come in forms of modern integration frameworks. No solution can do it all, so you need to look for solutions that can easily connect to other systems through flexible and powerful APIs.

- Insurance platforms making you faster at everything you do. This usually comes in the form of the support for the low-code paradigm and availably of no-code-low-code tools. You want to empower your people and leverage talent to create new products faster. Look for libraries of predefined content and support for the entire product life cycle.

- Self-sufficiency. You don’t want to wait for your vendor to code every little wrinkle in your process or products. Configuration solutions, such as AdInsure Studio, allow companies to tune and tweak every little aspect of the insurance platform.

- Insurance platforms offering easy process automation. This usually comes in the form of decision-making support which is embedded into every workflow used by different kind of platform users i.e. powerful business rules engine, integration with external data and models to make smarter decisions and automate processes.

- Platforms supporting innovation. Sometimes the best innovation happens when you get more people involved. For example, using APIs, you can make your data and processes available to outside communities for hackathons to create exciting new innovations. To do this, you need an open and flexible platform that can be extended securely.

Our own track record with AdInsure

Let’s talk a bit about our actual experience with the digitalization of insurance processes. One of our clients used AdInsure to digitalize the claims and policy management processes on a single IT system. As a result of the project, the average employee productivity working on claims settlement has improved by 112%. Before the process modernization, a single employee settled 86 claims per measurement period and after two years in production, this number has risen to 182 claims. This translates to a more than 50% reduction in the operational cost of handling a claim.

However, the benefits of digital transformation don’t stop there. Paperless document workflows mean that the company was able to roll out automated control over compliance with approved business processes. The system can generate reports about settlements of losses with minimal employee effort, providing improved insight into operations.

Communication with customers and partners has also improved. Clients can receive an SMS when their documents are ready and partners receive automated messages about settlements of losses. All this adds up to a far more efficient process that now delivers more value to the company.

Now, let’s circle back to the claim about cutting the cost of your claims journey by up to 30% we made at the start of this post. It is a feasible goal that you nevertheless need to approach strategically. For digital transformation success, you need to look at your entire value chain and identify the best opportunities for deploying technology.

These opportunities are everywhere. You might digitalize the initial claim capturing process with chatbots. Going paperless across the entire process is another option. There’s fraud detection or deep algorithmic reporting that uncovers hitherto hidden patterns.

And after you find the right one, you will be able to target your digitalization efforts on high-value areas that will power your business growth in the long term. This is what digital transformation is all about.