European insurers are modernising fast and the decisions they make now will define their competitiveness for the next decade. Adacta's 2025 State of Insurance Legacy System Modernization Survey reveals where the industry is heading, what systems are being prioritised, and how leading insurers are approaching the shift to modern cloud-based platforms.

At Adacta, a leading vendor of core systems for the insurance industry, we are committed to understanding and addressing the challenges of insurance organizations across Europe. Following our previous blog post, which explored the limitations of existing core systems, the key drivers of change, and the diverse internal perspectives on modernization based on the initial sections of our 2025 State of Insurance Legacy System Modernization Survey, we now turn our attention to the subsequent stages of this crucial transformation.

In this second blog, we will delve into the findings from sections four through six of our survey. These sections provide valuable insights into the progress being made in core system overhauls, the specific systems receiving the most modernization attention, and the varied strategies being employed by insurers as they navigate their modernization journeys.

Table of contents:

- The Current Momentum: Progress and Plans for Insurance Platform Modernization

- Identifying Key Targets: Insurance IT Modernization Priorities for Core Insurance Systems

- Charting the Path: Modernization Approaches for Core Systems

- Traditional vs. SaaS Mode: the growing interest for Cloud-based platforms

The Current Momentum: Progress and Plans for Insurance Platform Modernization

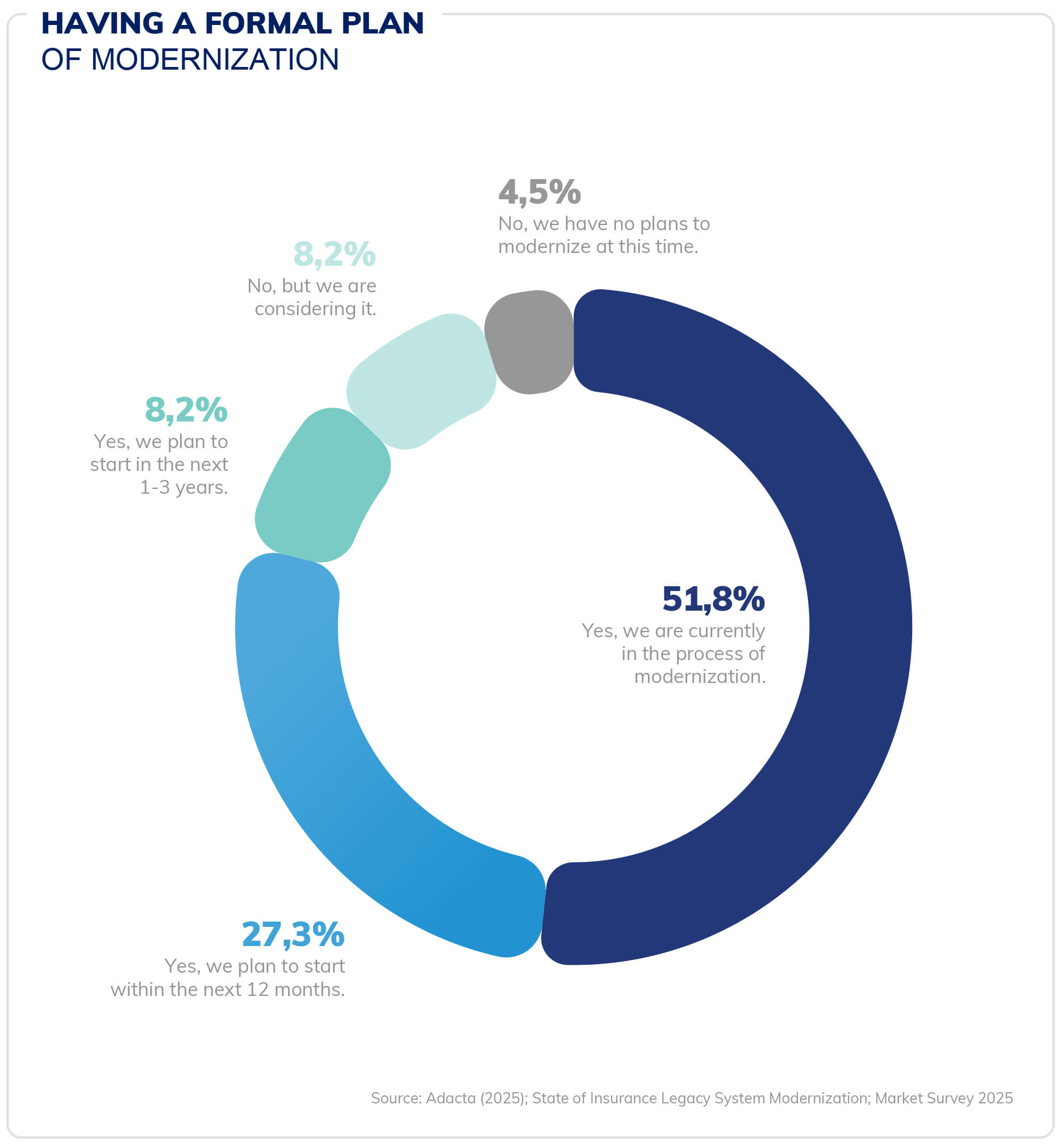

Our survey reveals that just slightly over half (51.8%) of surveyed organizations are currently engaged in core system modernization projects. Furthermore, 27.3% of respondents plan to initiate modernization efforts within the next 12 months, indicating a clear pipeline of future modernization activities. This strong level of activity underscores the industry's recognition of the urgent need to modernize to maintain a competitive edge.

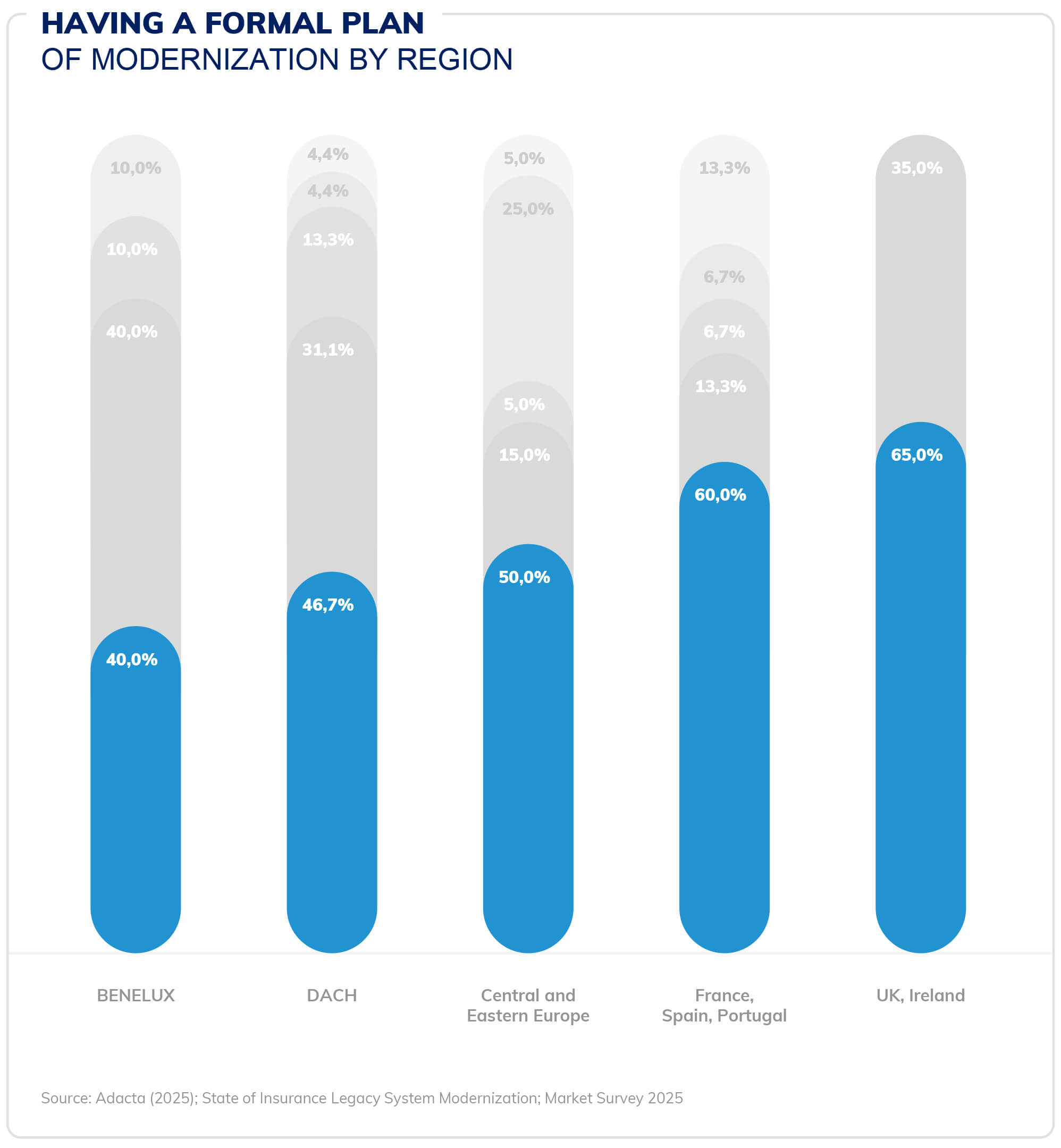

However, the pace of modernization varies across Europe. Our findings show that the UK and Ireland are leading the way, with all respondents either currently modernizing or planning to start within the next year. Similarly, France, Spain, and Portugal demonstrate high levels of engagement in modernization.

In contrast, while Continental Europe, including the CEE, Benelux, and DACH regions, shows a strong intent to modernize, a portion of organizations in these areas are still in the planning stages or anticipate longer timelines. This regional divergence likely reflects varying market pressures and specific local challenges.

Identifying Key Targets: Insurance IT Modernization Priorities for Core Insurance Systems

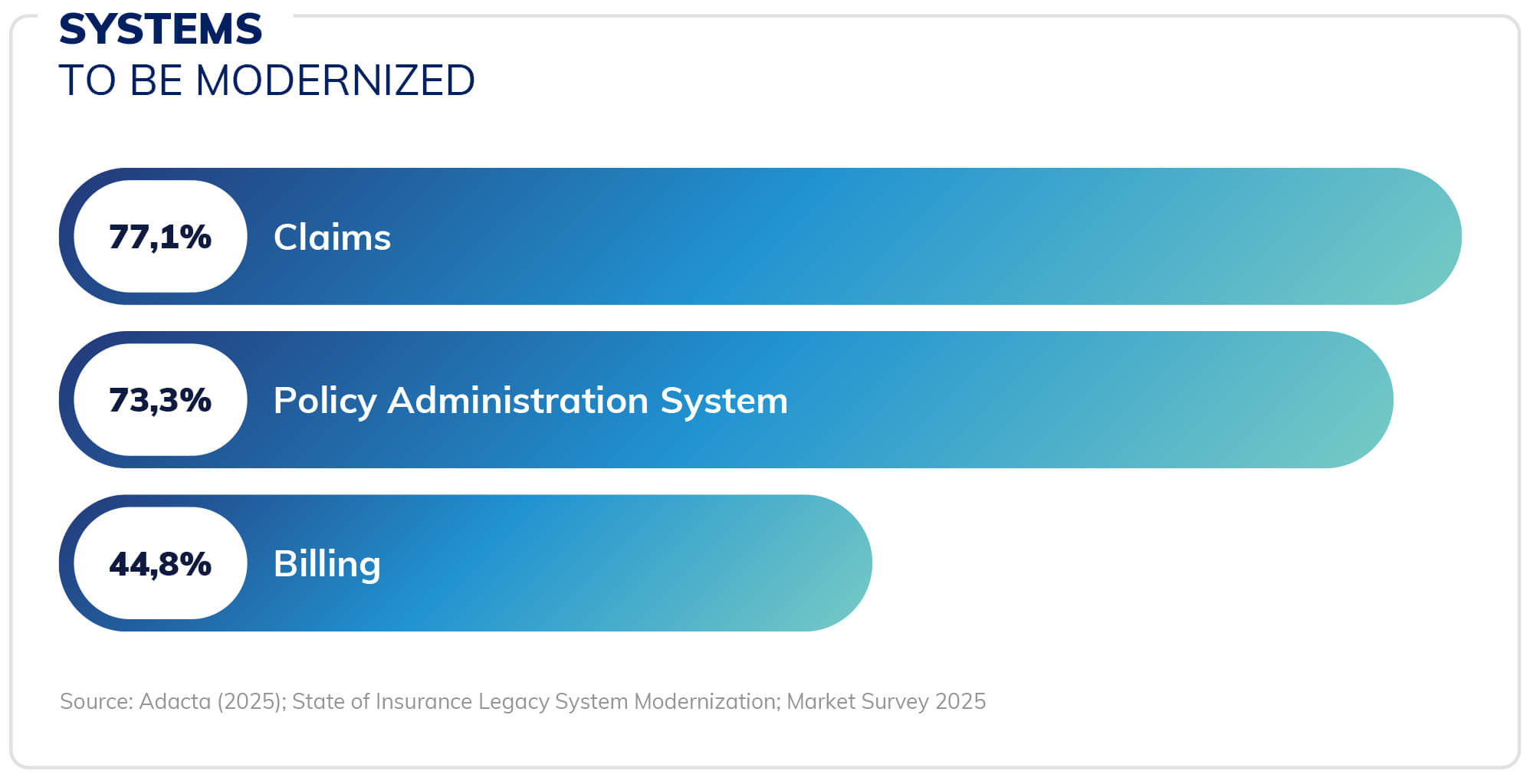

When it comes to priorates for business process modernization across the insurance value chain, our survey data indicates that claims systems are the top priority, with 77.1% of respondents planning upgrades. The focus on claims is understandable, as it represents a critical customer touchpoint and often the largest operational expense for insurance companies. Modernizing claims systems aims to enhance operational efficiency, improve customer experience through faster handling, and ultimately cost reductions.

Following closely, policy administration systems (PAS) are also a significant modernization target, with 73.3% of respondents planning upgrades. Upgrading PAS is often driven by the need to support new products, improve time-to-market, and enhance overall business agility.

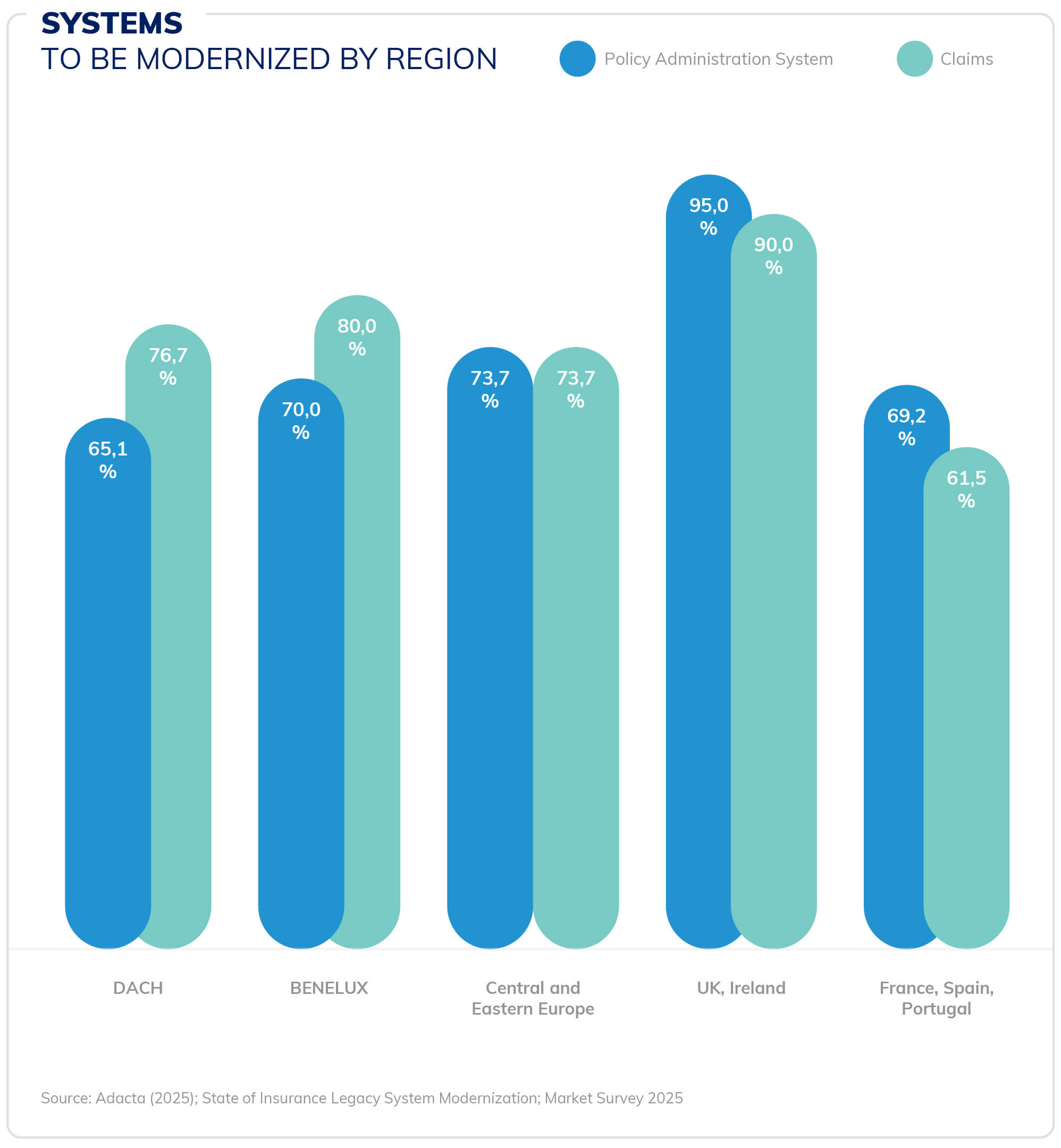

Interestingly, we observed regional variations in the prioritization of claims versus PAS. While claims modernization is on average the highest priority across most regions, insurers in the UK and Ireland, as well as France, Spain, and Portugal, show a stronger emphasis on PAS upgrades. This suggests a potential regional focus on driving new business growth in these markets. Billing systems, on the other hand, appear to be a lower priority, with less than half (44.8%) of respondents planning upgrades.

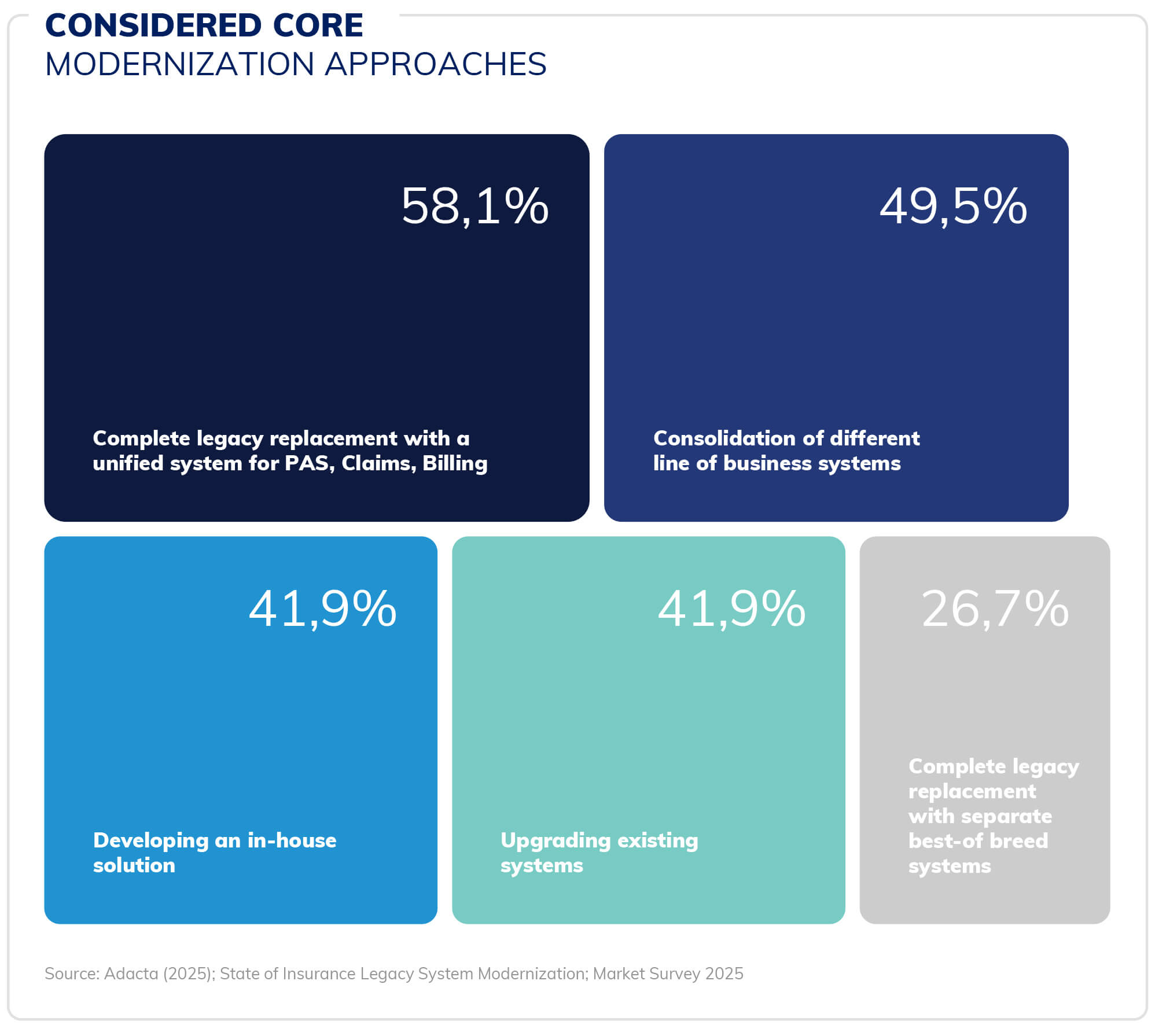

Charting the Path: Modernization Approaches for Core Systems

In terms of how insurers are approaching modernization, our survey reveals a preference for a comprehensive consolidation. The leading approach, favored by 58.1% of respondents, is a complete legacy replacement with a single unified system encompassing policy administration, claims, and billing. This indicates a strong desire to consolidate operations, reduce complexity associated with fragmented legacy environments, and streamline vendor management.

Consolidation of different lines of business systems is another significant approach, considered by 49.5% of respondents. This strategy aims to simplify complex IT landscapes and improve data consistency. Interestingly, developing in-house solutions (41.9%) and upgrading existing systems (41.9%) are also being considered by a substantial portion of insurers, reflecting diverse strategic choices based on internal capabilities and specific requirements.

Traditional vs. SaaS Mode: the growing interest for Cloud-based platforms

When it comes to modernization models, our survey highlights a significant trend in the adoption of the SaaS (Software as a Service) models for core systems, with just over half (50.5%) of new modernization initiatives opting for a SaaS deployment. This shift towards cloud-based solutions (including private cloud and hybrid cloud) signifies a growing acceptance of the benefits of SaaS, such as scalability and reduced infrastructure management.

We observed a particularly strong preference for SaaS among insurance intermediaries (MGAs, Brokers), with 65.2% considering this approach, likely driven by their agility and openness to innovation. P&C carriers (47.9%) show a more balanced adoption, while life insurers (44.1%) appear more cautious in migrating core workloads to the cloud, potentially due to the long-term nature of their products and stringent regulatory requirements.

These insights from sections four through six of our 2025 survey paint a clear picture of an industry actively engaged in and planning for significant core system modernization driven by the digital transformation of the insurance sector. At Adacta, we are committed to providing the expertise and solutions necessary to support insurers on these complex yet critical journeys. Stay tuned for our next blog post, where we will explore the main barriers that insurance organizations face when undertaking core system modernization.