What are the key findings of the 2025 State of Insurance Legacy System Modernization Survey?Inflexibility, high maintenance costs, and integration challenges are the biggest limitations holding insurers back from digital transformation. According to Adacta's 2025 survey, nearly half of insurers cite legacy system obsolescence as the primary trigger for modernization, alongside regulatory compliance pressure and rising customer expectations. While innovation and operations teams champion change, finance and compliance departments remain cautious — making internal alignment one of the biggest hurdles to successful core system replacement.

At Adacta, a leading vendor of modern insurance core systems, we work closely with insurance organizations on legacy insurance system modernization projects. Recognizing that outdated legacy systems pose a significant barrier to digital transformation, we sought to gain deeper insights into the challenges and opportunities faced by the industry. That’s why we designed and performed the 2025 State of Insurance Legacy System Modernization Survey—to capture firsthand perspectives from industry leaders and understand the drivers and inhibitors of change.

In a series of blog posts, we will outline the findings of our research. This first blog post highlights the key findings from the first three sections of our survey, shedding light on the limitations of existing core systems, the driving forces behind modernization, and the diverse perspectives of key stakeholders.

Table of contents:

- Unmasking the Constraints: Main Limitations of Existing Core Systems

- The Catalysts for Change: Key Drivers of Legacy Insurance System Modernization

- Valuable Insights on Internal Perspectives: Key Stakeholders' Stance on Legacy Modernization

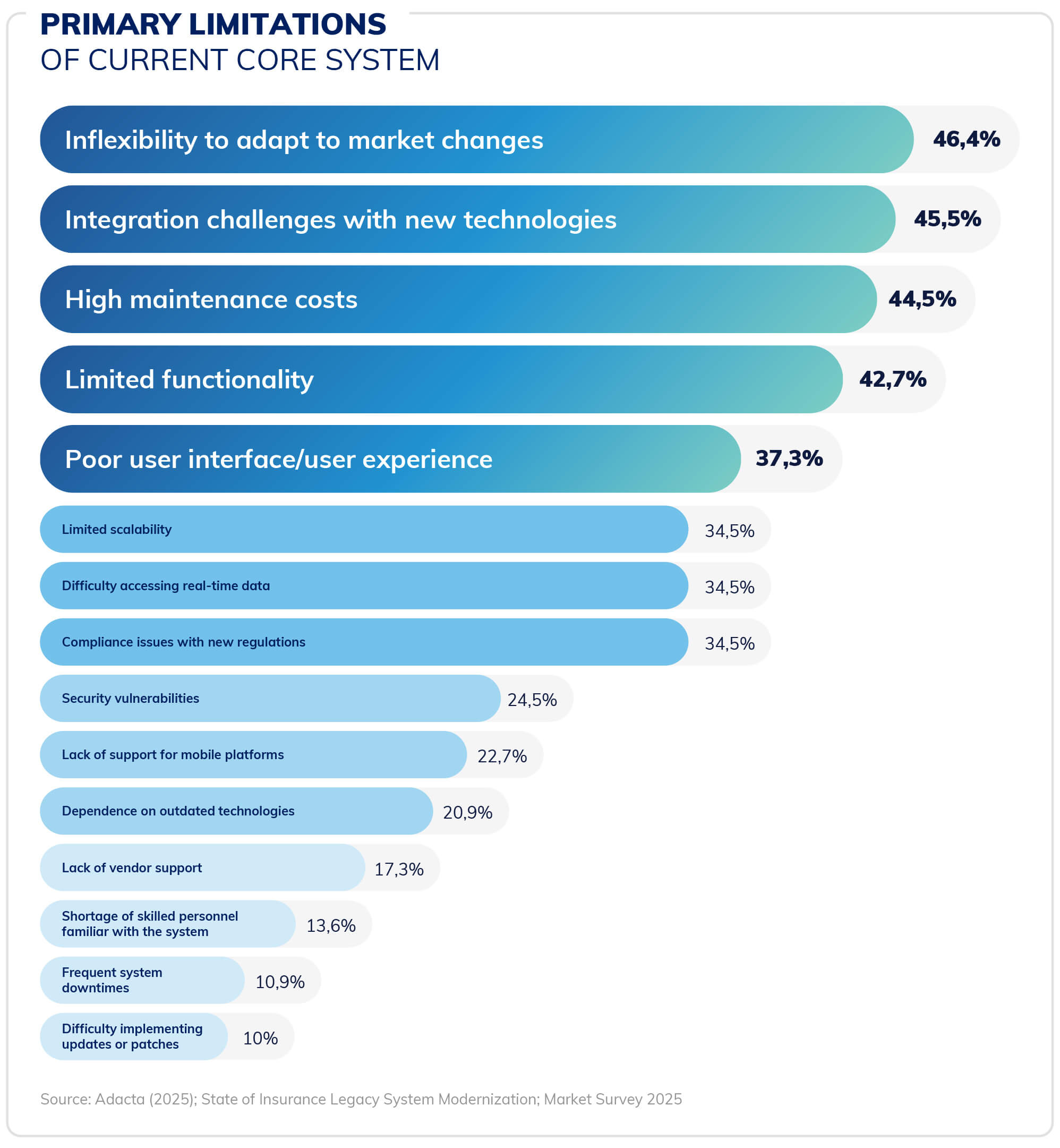

Unmasking the Constraints: Main Limitations of Existing Core Systems

Our survey revealed that the inflexibility to adapt to market changes is the most significant limitation of insurers' current core systems, cited by 46.4% of respondents. This lack of agility hinders their ability to respond effectively to evolving customer expectations and competitive pressures. Closely following this, integration challenges with new technologies (45.5%) and high maintenance costs (44.5%) were also identified as major pain points.

The struggle with integration highlights the increasingly interconnected nature of the insurance industry, where seamless data exchange and system compatibility are crucial for innovation and operational efficiency. Outdated legacy technology often becomes bottlenecks, preventing the adoption and seamless integration of new digital tools. Furthermore, the age of these legacy systems, often between 13 and 15 years, leads to escalating maintenance issues and expenses, diverting valuable resources from strategic initiatives.

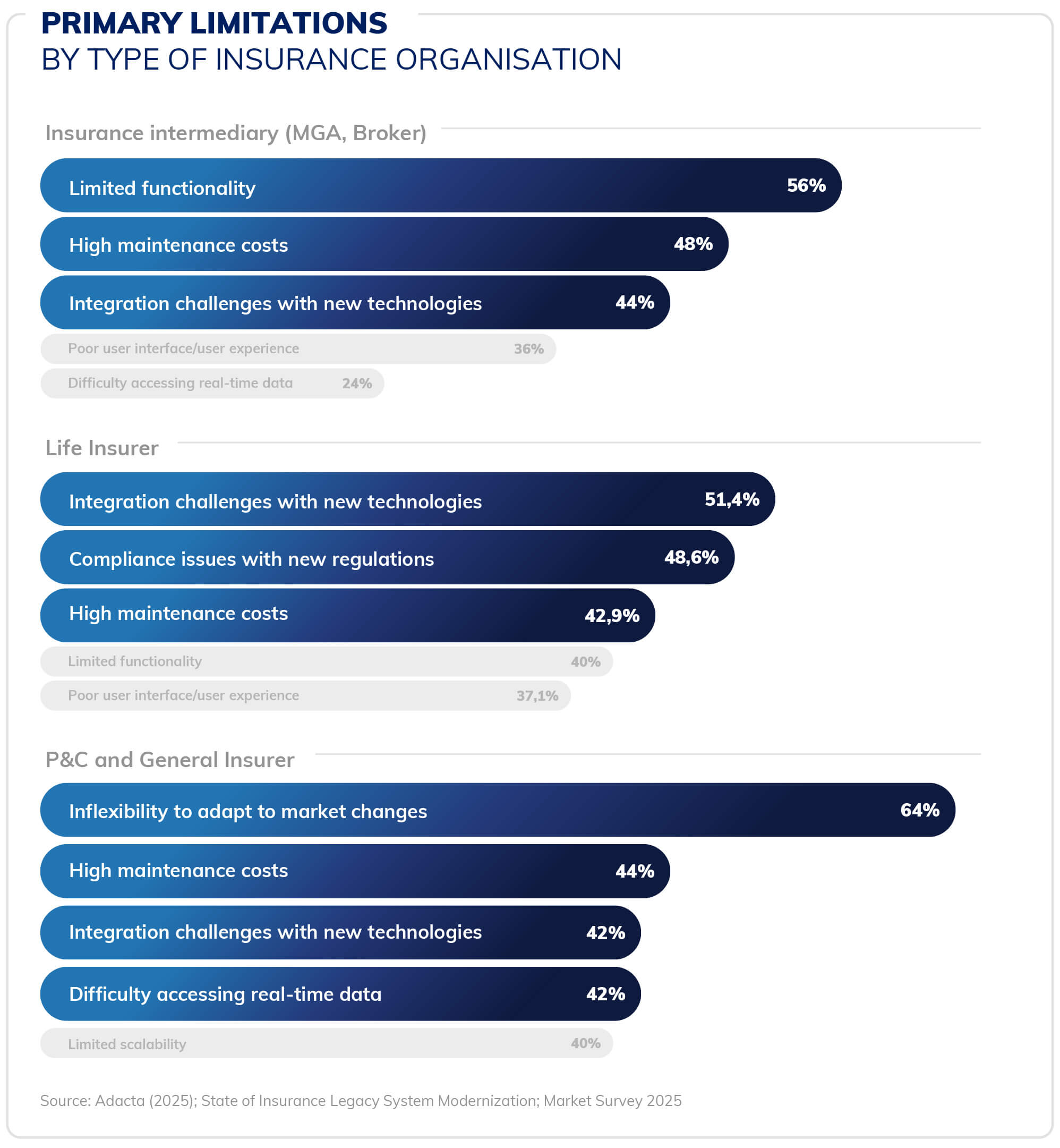

Interestingly, the primary limitations also vary depending on the type of insurance company:

- P&C and General Insurers rank inflexibility to adapt to market changes as their top obstacle (64%)

- Insurance intermediaries (MGAs, Brokers) point to limited functionality as their primary challenge (56%)

- Life Insurers struggle most with compliance issues with new regulations (48.6%)

Despite these differences, high maintenance costs and integration challenges with new technologies are common struggles faced by all types of insurance organizations. These findings underscore the urgent need for modern technology to overcome these fundamental limitations that hinder business objectives.

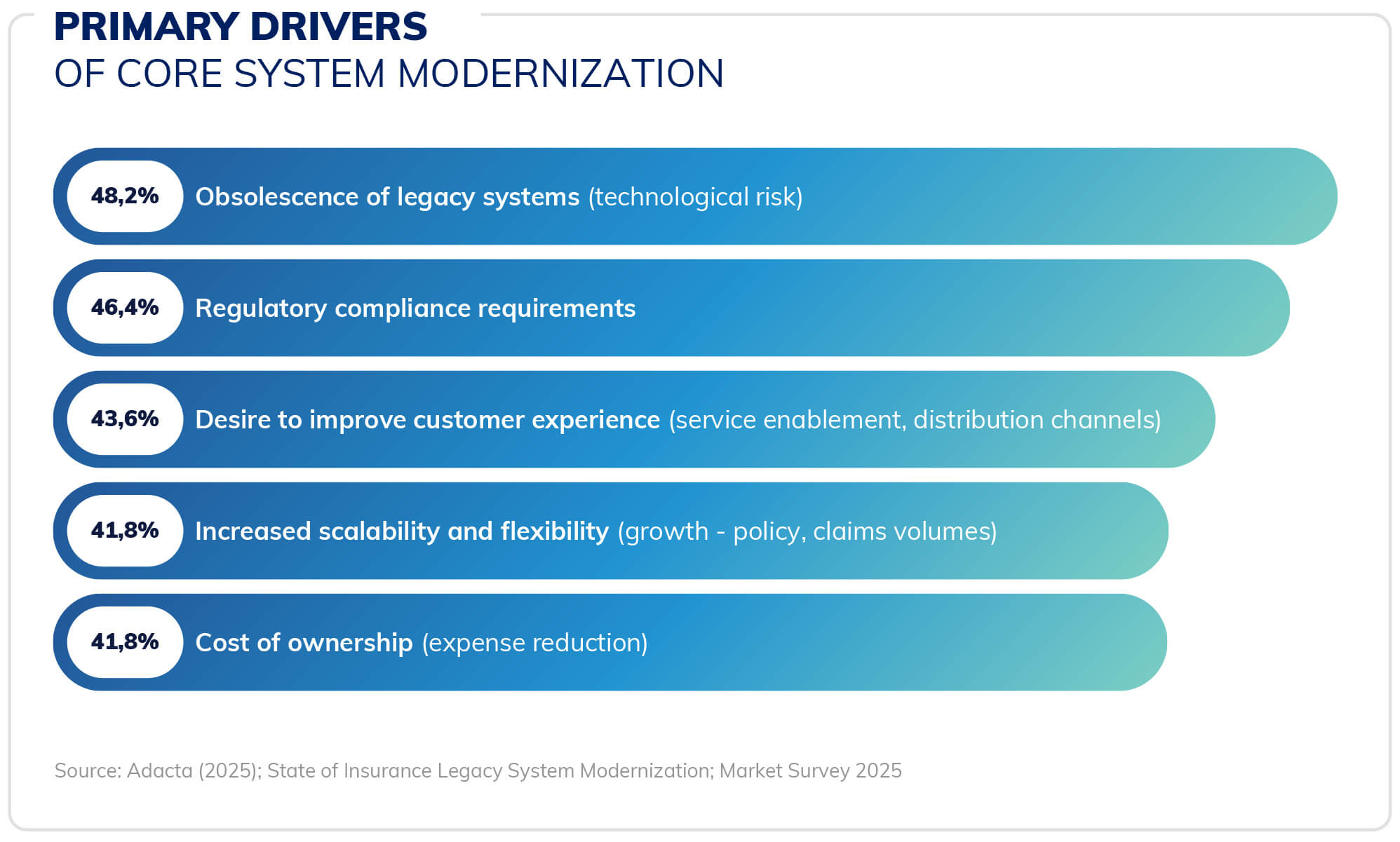

The Catalysts for Change: Key Drivers of Legacy Insurance System Modernization

The survey clearly indicates that the obsolescence of legacy systems is the primary trigger for core system modernization, cited by nearly half of the respondents (48.2%). As these outdated systems become increasingly complex and costly to maintain, and as they fail to support new business requirements, organizations are compelled to seek modern alternatives.

Following closely, regulatory compliance requirements (41.8%) and the desire to improve customer experience (43.6%) are also significant drivers. The evolving regulatory landscape necessitates system upgrades to ensure adherence. At the same time, the increasing customer demands and expectations of digitally savvy customers require more efficient and personalized services, pushing insurers to modernize their core operations.

While factors such as the cost of ownership (41.8%) and the need for increased scalability and flexibility (46.4%) also play a role, many insurance organizations approach core system replacement with caution due to the perceived significant risks involved. Often, modernization is only initiated when technology failures or regulatory demands leave them with no other choice.

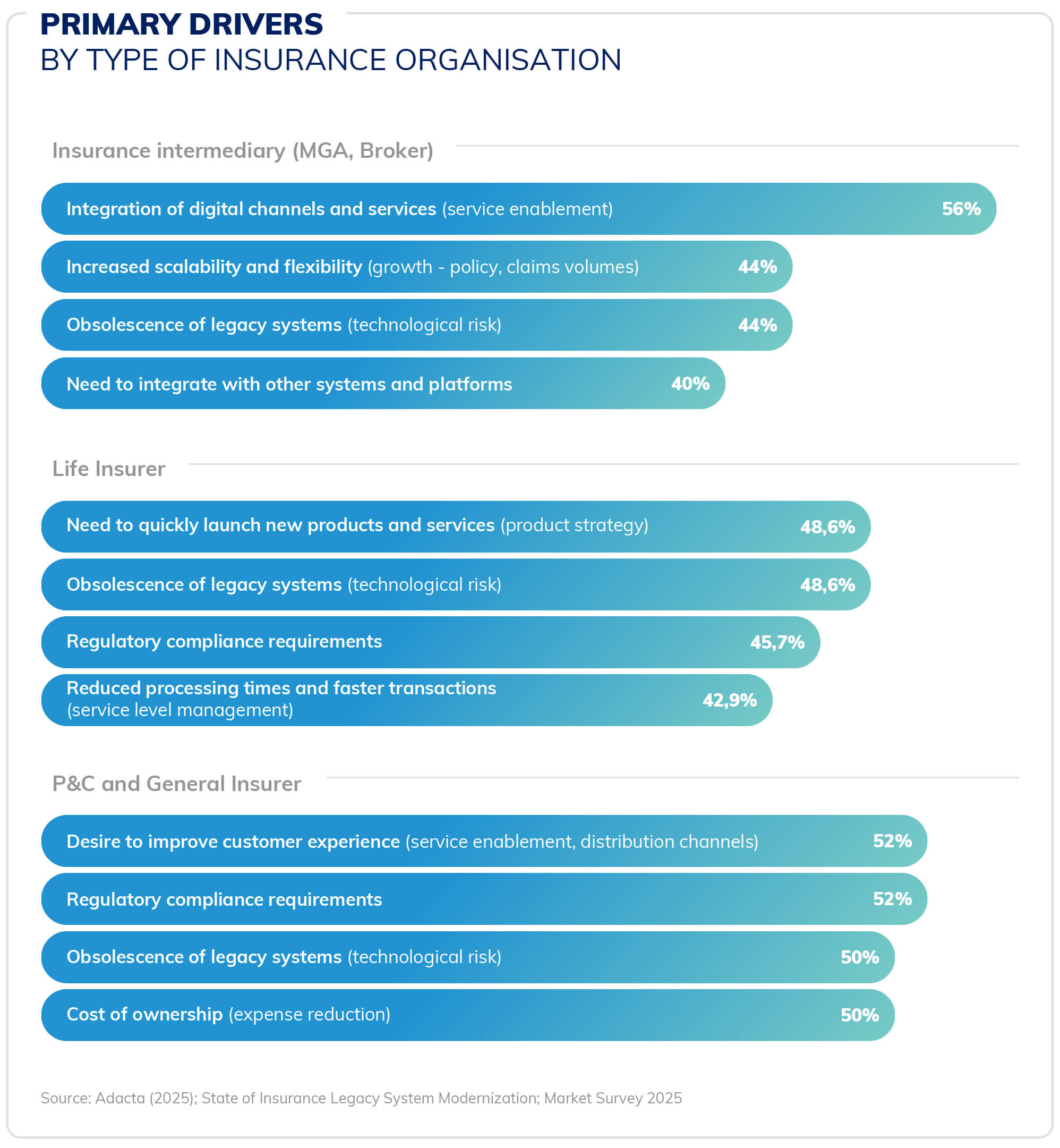

The primary drivers also show variations across different types of insurers.

- For insurance intermediaries, the biggest motivator is the integration of digital channels and services (56%), followed by increased scalability and flexibility (44%)

- Life insurers place equal emphasis on short time-to-market (48.6%) and obsolescence of legacy systems (48.6%), with regulatory compliance requirements also being a high priority (45.7%)

- In the P&C sector, customer experience and regulatory compliance tie as the leading drivers (both 52%), with roughly half also prioritizing expense reduction and managing technological risk

Valuable Insights on Internal Perspectives: Key Stakeholders' Stance on Legacy Modernization

Given the complexity and risk associated with core system modernization, internal stances and support for these initiatives vary considerably across different roles. Our survey revealed a spectrum of perspectives, from enthusiastic advocates to cautious observers.

Leaders in innovation, marketing, digital transformation, and operations are generally the most enthusiastic supporters of modernization. Their enthusiasm is fueled by the potential for growth, efficiency, and gaining a competitive advantage. They recognize that modern systems can unlock new opportunities, improve customer satisfaction, and ultimately provide a competitive edge.

In contrast, finance, legal, and compliance departments tend to approach modernization with greater caution. Their hesitation, based on their roles, often stems from concerns over costs, potential security risks, and the complexities of navigating regulatory requirements during and after the modernization process.

The views of IT leaders and board members are more nuanced, displaying both support and resistance. Some IT heads favor modernization to enable the adoption of advanced technologies, while others face challenges due to the constraints of existing systems. Board members often express concerns about potential operational disruptions during the implementation phase, highlighting the need for careful planning and risk mitigation.

Understanding these diverging internal perspectives is crucial for successfully navigating the complexities of legacy platform modernization. Building consensus and addressing the concerns of all key stakeholders are essential steps towards a smooth and effective transformation.

Stay tuned for our next blog post, where we will delve into the progress and plans for core system overhauls across the European insurance landscape.